The Biofuel Decade

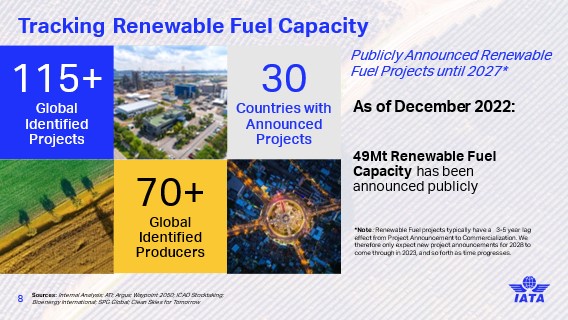

Aviation’s immediate decarbonisation priority is to continue the sector’s Sustainable Aviation Fuels (SAF) ramp-up, which for at least the next decade, will be derived from Biofuels. In 2022, between 250-350,000t of SAF will be produced which, when juxtaposed against the 24,000,000t tipping point identified for 2030, portrays a long road ahead. However, as represented in the figure below, the next 5 years will pose a marked shift in the SAF production landscape, where we can anticipate a diversification of producers, production pathways and feedstocks.

Aviation is on the cusp of leveraging new inputs to complement today’s predominant output of 2nd generation feedstock based SAFs produced via the HEFA pathway. This is important given that feedstock typically constitutes 60-80% of a SAF’s production cost. The feedstock is the core driver of how SAF is measured through its ability to avoid or capture carbon through its collection or growth.

The exciting aspect of 3rd generation, waste-based feedstocks, is their associated positive socio-economic externalities, from the mass clearing of methane-emitting urban-landfill to the re-purposing of agricultural or forestry biomass otherwise sent for incineration or landfill. This could create an ability to produce negative carbon-intensity and nature-positive outcomes with an additional social benefit.

To fully realise the potential of these feedstocks and drive aviation's energy transition forward, there's still a need for governments to implement policy frameworks that will work to reduce the opportunity cost of SAF production and prioritize SAF over other biofuels. In absence of policy incentivizing SAF production, it will face lower percentage cuts relative to co-products like renewable diesel, as biorefineries will optimise their output around fuels offering higher margins. Whilst ensuring demand helps to generate investor confidence, mandate-style policies in absence of production incentives will fail to address aviation's need to scale SAF supply.

Looking Toward Zero Carbon Flying

SAF require two main ingredients for their manufacture: Carbon and Hydrogen. Hydrogen can also become a carrier of renewable energy to be used as fuel on its own, with near-zero carbon throughout its life cycle if manufactured with renewable energy. The use of hydrogen for aviation has already started at small scale:

This is the tailwind the sector needs to start tackling the challenges that a zero-carbon fuel will have, such as the scalability of hydrogen, the development and maturing of key enablers, and the scaling-up of renewable energy to manufacture the fuels.

Analogous to the electrification of road transport or the deployment of renewable energy, hydrogen for aviation could unlock a complete shift in air travel, reducing CO2 emissions, improving local air quality and opening possibilities for local fuel production in all the world regions. While large scale hydrogen aircraft are still more than a decade away, the work to prepare for this in terms of technology, infrastructure, regulations and certification must start today.

Daniel Bloch and Dr. Alejandro Block

IATA