Annually since 2005, McKinsey has analyzed the aviation value chain.

We look at participants from across the value chain, including airlines; OEMs that produce aircraft and engines; aircraft lessors; air navigation service providers; jet fuel producers; airports; catering suppliers; ground services companies; maintenance, repair, and overhaul organizations; freight forwarders; and providers of global distribution systems and other travel technologies. We analyzed the financial performance of the aviation value chain through the lens of economic profit, defined as the difference between the return on invested capital (ROIC) and the alternative return from equal-risk opportunities that investors can access.

As a whole, the aviation value chain recorded an economic loss of roughly $14 billion in 2024. By comparison, the average annual loss in the prepandemic period from 2012 to 2019 was approximately $10 billion and 2023’s loss was only $6 billion.

The sectors with the largest profits in 2024 were freight forwarders, aircraft lessors, and global distribution systems (which are centralized reservation systems that connect airlines with travel agents and other ticket distributors around the world). Airlines suffered large losses in absolute terms, just as they did in 2023. Six of the eleven subsectors we track showed positive economic profit.

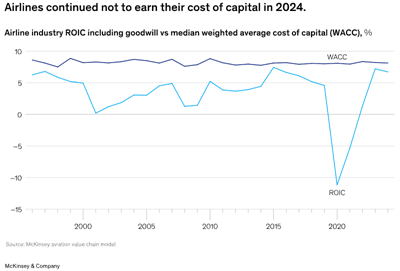

Although airlines’ collective economic performance continued to be better than the 2012 to 2019 average, our analysis shows that the airline sector’s ROIC remained below the weighted average cost of capital in 2024—as has been the case dating back to at least 1996. The share of value-creating airlines in our sample was 36 percent—above the longer-term trend but lower than in 2023, when 46 percent of our airline sample was value creating.

Year-over-year demand growth (measured through revenue passenger kilometers flown) was a robust 10.6 percent in 2024. Demand outgrew supply, with year-over-year growth in available-seat kilometers flown at 8.8 percent. Cargo yields dropped, but cargo revenue remained at roughly 150 percent of what it was in 2019.

2025 appears to be a mixed picture for airlines. Geopolitical tensions have led to uncertainty. Changes in tariffs have affected cargo flows. On the positive side, demand—especially premium demand—remains strong. Passengers appear willing to pay for better experiences. The composition of premium cabins has also changed over time, with an increased share of leisure travelers sitting at the front of the plane. Business class and first class passenger revenues from January through September of 2025 were up about 3.5 percent compared with the same period in 2024, and revenue increased 3.3 percent for all classes combined. Meanwhile, the price of jet fuel, which represents the largest single cost item for airlines, is (as of early November 2025) down about 9 percent from 2024 levels and down about 22 percent from 2023 levels.

The full analysis dives deeper into the various aspects of the performance of the aviation value chain.

Authors:

![]()

*Find out more about McKinsey & Company's engagement in the IATA's Strategic Partnership Program on the partners directory.