Need Help?

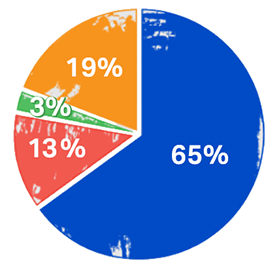

The aviation sector has committed to achieving net zero carbon emissions by 2050. Delivering this ambition will require a combination of technological innovation, operational improvements, and policy support, with sustainable aviation fuel (SAF) representing the most impactful solution in the coming decades: it could contribute up to 65% of the reduction in emissions needed by aviation to reach net zero CO2 emissions by 2050.

What is SAF?

SAF is an alternative to conventional aviation fuel. It can be made from many different sustainably sourced materials, such as used cooking oil, biomass waste and residues, and renewable energy and carbon. SAF can significantly reduce lifecycle carbon emissions, typically by around 80% compared to conventional aviation fuel.

SAF is safe, certified, and already in use on commercial flights today. As a drop-in fuel, it can be blended with conventional aviation fuel and readily used without requiring any modifications to aircraft or airport infrastructure.

> Frequently Asked Questions on SAF

> Fact sheet: SAF (pdf)

The SAF Challenge

Scaling SAF production so that the cost can come down is a key challenge for this new energy market. SAF currently represents less than 1% of global aviation fuel use, and it is several times more expensive than conventional aviation fuel. This is the result of more expensive feedstocks, still developing production technologies, lack of physical and market infrastructure, and high upfront investment needs.

As with the wind and solar energy markets when they were new, addressing these challenges will require supportive government policies, a coherent strategy across the wider energy system, and close collaboration across the aviation value chain. A strategically sequenced, energy-system-wide approach to new energy market policies can help accelerate decarbonization across sectors, including aviation.

Watch the media briefing on sustainability held in June 2026 during IATA's 82nd AGM in Rio de Janeiro, including an update on SAF.

> Access the full presentation (pdf)

Publications

Need Help?

")

SAF Facilities & Policies

Announced SAF Facilities

The map below highlights renewable fuel facilities that produce or plan to produce SAF worldwide, showing both existing and emerging SAF capacity and technology pathways. Note that SAF capacity does not equal actual production, SAF is only one of several outputs from any refinery, and not all announced capacity will materialize. SAF technologies include Hydroprocessed Esters and Fatty Acids (HEFA), HEFA co‑processing, Gasification Fischer–Tropsch (GFT), Alcohol‑to‑Jet (AtJ), Power‑to‑Liquids (PtL), and other emerging technologies (other).

The data includes publicly announced projects and provides key details, including location, technology, SAF capacity, expected start-up year, and project status (announced, under construction, or operating). Projects still in early stages or lacking sufficient public information are excluded. The map does not assess whether projects will be completed or evaluate their likelihood of success.

The SAF facilities data covers disaggregated production capacity – not actual SAF production.

- A high portion of the identified SAF capacities will not materialize, as many projects are unlikely to reach final investment decision (FID) to start production, based on past observations across renewable fuels, SAF, and other emerging energy sectors.

- SAF capacity represents the maximum theoretical annual SAF production capability. The design capacity may not be fully reached, and facilities may operate at lower utilization rates due to technical or economic constraints. In addition, all facilities produce a mix of products, such as SAF, renewable diesel, and naphtha, and refiners may choose to favor other products over SAF in their product slate.

Supportive policy conditions largely determine whether projects succeed, how much SAF capacity materializes, and whether companies choose to produce SAF; as a result, the data shows what could be achieved under favorable policy and market conditions.

If you identify missing or inaccurate information, or wish to share updates, please contact us at economics@iata.org.

SAF Policies

IATA closely monitors policies that are planned or adopted to support SAF production and use. While these policies share common objectives of enabling the airline industry to decarbonize, countries have taken different approaches to policy design and implementation. Several countries have also set SAF targets that will serve as a foundation for future policies to accelerate SAF deployment. Obliged parties and beneficiaries also vary across these policies. Click on a country to explore its SAF policies that are planned or implemented.

If you identify missing or inaccurate information, or wish to share updates, please contact us at economics@iata.org.

How IATA Supports SAF Scale-Up

IATA actively supports the scale-up of SAF through analysis, solutions, and extensive partnerships in the industry and beyond.

IATA developed the Net Zero Roadmaps 2050 that chart the path to net zero by covering aircraft technology, energy, operations, finance, and policy. Our research covers SAF feedstocks and production technologies, lifecycle emissions, non-CO2 effects, fuel supply and demand, infrastructure needs, policy frameworks, financing barriers, and the role of emerging technologies, including carbon capture.

IATA works to promote the most effective policy measures when it comes to building new energy markets. Policies must integrate operational realities as they pertain to our uniquely multi-jurisdictional industry. Harmonization, simplification, and competition-neutrality are all essential for delivering the greatest possible emissions reductions at the lowest possible cost.

IATA collaborates with governments and international bodies such as the International Civil Aviation Organization (ICAO) to this end and supports the implementation of global mechanisms such as CORSIA to accelerate SAF deployment.

IATA launched the Civil Aviation Decarbonization Organization (CADO) that operates a SAF registry to accelerate the scaling of the SAF market: the CADO SAF Registry. Without a SAF registry, the market would remain local until the infrastructure that can make the market global arrives. This global system is open to all SAF value chain stakeholders and manages the chain of custody of SAF environmental attributes, ensuring that these are transparently tracked across the value chain and can be credibly claimed under both regulatory obligations and voluntary schemes by airlines and their customers.

On the procurement side, the IATA SAF Matchmaker facilitates early-stage SAF transactions by connecting airlines with SAF producers, matching supply offers with demand and improving market visibility for early commercial engagement.

Together, these solutions reduce transaction complexity, build market confidence, and support the development of a more scalable global SAF market.

SAF Documentation

Frequently Asked Questions (FAQ)

Understanding SAF

What is Sustainable Aviation Fuel (SAF)?

SAF is a non-fossil fuel for use in aircraft. It can be produced from many different sustainably sourced materials called feedstocks, such as used cooking oil, biomass waste and residues, and renewable energy and carbon. These materials can be converted using multiple technology pathways, and lifecycle carbon emission reductions vary by fuel type.

To qualify under international sustainability frameworks, SAF must meet stringent sustainability and lifecycle emissions-reduction criteria, such as those set by the International Civil Aviation Organization (ICAO) under its Carbon Offsetting & Reduction Scheme for International Aviation (CORSIA) framework.

IATA estimates that Sustainable Aviation Fuel (SAF) could contribute up to 65% of the reduction in emissions needed by aviation to reach net zero CO2 emissions by 2050.

Today, most SAF production uses waste- and residue-based feedstocks through the Hydroprocessed Esters and Fatty Acids (HEFA) pathway, typically delivering lifecycle emissions reductions of around 80% compared to conventional aviation fuel. Emerging technologies and new feedstocks have the potential to increase lifecycle emissions reductions above 90%, even achieving negative emissions on a lifecycle basis.

In addition to reducing emissions, SAF can strengthen a country’s energy security by diversifying the energy supply and building domestic fuel production from locally available resources. SAF can also support economic growth by driving investment in agriculture, waste management, renewable energy, and advanced fuel technologies, and create new jobs across all these new industries.

How is SAF produced?

SAF is produced worldwide using a range of feedstocks and technologies. Today, 11 SAF production pathways are certified under American Society for Testing and Materials (ASTM) standards, allowing SAF to be safely blended with conventional aviation fuel and used in existing aircraft and infrastructure.

These pathways fall into two main categories: bio‑SAF, which is produced from sustainably sourced biomass feedstocks; and e‑SAF (electro‑SAF), also referred to as power‑to‑liquid (PtL) SAF, which is made using renewable electricity, typically by combining green hydrogen with captured carbon dioxide.

For additional information on how SAF is produced, refer to the IATA SAF Handbook and IATA's Global Feedstock Assessment for SAF Production.

What is SAF made from?

SAF can be made from different renewable and waste-based feedstocks. These can range from existing crop species to more novel options such as waste and residues. Which feedstocks to use depends on the geographic location, with different regions more suited to certain types of feedstocks. SAF produced in one part of the world can be entirely different from SAF produced elsewhere, depending on the inputs. Although the origins of SAF may vary across regions, the alignment of fuel with internationally recognized sustainability criteria – such as the ICAO CORSIA framework – means that the resulting fuel will be harmonized in terms of sustainability and technical standards.

Typical SAF feedstock examples include:

- Fats, oils, or grease: these can be sourced from waste, such as used cooking oil and animal fat, or virgin oils produced from a variety of edible and non-edible crops.

- Sugars and starches: these include feedstocks such as sugarcane and corn, as well as more novel sources like agricultural residues and other non-food plant materials.

- Solid biomass such as municipal solid waste (MSW), waste wood, and forestry residues.

- Non-renewable waste or exhaust gases: these are fossil wastes that are no longer suitable for recycling, or waste gases generated by industrial production processes.

What is the most used SAF today?

The vast majority of SAF produced today is bio‑SAF, primarily using hydroprocessed esters and fatty acids (HEFA) technology. HEFA converts waste oils and fats, such as used cooking oil or animal fats, into jet fuel through a process similar to conventional oil refining. As the most mature and commercially available pathway, HEFA is currently the most cost‑effective way to produce SAF. However, HEFA is limited by feedstock availability, and new SAF pathways are required to enable decarbonization at scale.

Benefits of SAF

How does SAF help reduce aviation carbon emissions?

SAF helps reduce aviation carbon emissions by replacing conventional aviation fuel with fuel made from renewable or waste-based sources. SAF produces similar emissions to aircraft exhaust, because fuel is still being combusted. This will be the case until such time that novel aircraft propulsion systems, such as hydrogen, become a reality. SAF’s climate benefit comes from how it is produced using waste, residues, or recycled carbon instead of fossil oil. Thanks to the non-fossil origin of SAF inputs, fossil-derived carbon emissions will be reduced. Depending on the production method and the feedstock, the lifecycle greenhouse gas (GHG) emissions reductions of SAF can range significantly. Most of the current SAF supply comes from waste oils, reducing emissions by around 80% compared with conventional aviation fuel while remaining compatible with existing aircraft and airport infrastructure.

How important is SAF for aviation’s net zero CO2 goal?

SAF is expected to deliver around 65% of the emissions reductions needed for aviation to reach net zero CO₂ emissions by 2050. No other solution currently offers a greater potential impact on aviation’s decarbonization. Importantly, SAF can be used as a drop-in solution on existing aircraft we have today, enabling immediate emissions reductions without changes to aircraft or airport infrastructure.

What makes SAF sustainable, and how to ensure environmental integrity?

SAF is considered sustainable because it is produced from renewable or waste-based sources that can reduce lifecycle greenhouse gas (GHG) emissions significantly compared with conventional aviation fuel, while avoiding negative environmental and social impacts.

To ensure environmental integrity, SAF must meet strict sustainability criteria and certification requirements covering feedstock sourcing, land-use change, biodiversity protection, water use, and emissions accounting. International frameworks and certification schemes also require traceability and independent verification throughout the supply chain to ensure that SAF delivers genuine and credible environmental benefits.

Can SAF help reduce non-CO2 emissions and effects?

Yes. The aromatic or sulfur compounds in fossil-based conventional aviation fuel are responsible for the particulate emissions that contribute to contrail formation and poor air quality. Since SAF in its pure form doesn't contain any of these compounds, it can lead to cleaner fuel (i.e., with lower aromatic and sulfur content) when blended with conventional aviation fuel.

What are the broader benefits of SAF beyond aviation?

SAF can deliver broader benefits beyond reducing aviation emissions by supporting the development of renewable energy industries, creating jobs across fuel supply chains, and strengthening energy security through domestic production and diversification away from fossil fuels.

SAF production can also help promote circular economy solutions by converting waste materials such as used cooking oil, agricultural residues, and municipal waste into valuable energy resources. In addition, investments in SAF technologies and infrastructure can accelerate innovation in low-carbon fuels that may also benefit other hard-to-abate sectors beyond aviation, such as shipping and heavy industry.

Adopting and Scaling SAF

Is SAF safe to use in current aircraft?

Yes. SAF meets the same safety requirements as conventional aviation fuel for use in commercial aircraft. Fuel specifications ensure that both conventional aviation fuel and SAF meet the required chemical and physical standards. Throughout the distribution process, the fuel is regularly tested and monitored to ensure it remains safe, reliable, and fully compliant before being used in aircraft.

SAF has been used in commercial flights for many years, with millions of flight hours completed without safety issues. It is a “drop‑in” fuel, meaning it can be blended with regular jet fuel and used in existing aircraft, engines, and airport fuel systems without requiring any modifications to these.

Why is SAF more expensive than conventional aviation fuel?

SAF is more expensive than conventional aviation fuel primarily because it is produced at a much smaller scale and relies on newer, less mature production pathways. Unlike fossil jet fuel, which benefits from decades of large-scale production and established infrastructure, SAF is made from sustainably sourced materials that are often more costly and limited in supply. Converting these materials into SAF requires more complex processes, and many technologies are still in early stages of commercial deployment. This requires significant upfront investment while demand remains limited.

It is important to note that the price airlines pay for SAF (and for fossil jet fuel), in addition to production costs, includes many administrative add-on costs such as certification, transaction-related costs, and markups throughout the supply chain.

These add-ons may vary significantly: in 2024, the difference between production costs and market prices (the market premium) for HEFA SAF in Europe reached around 1,000 USD/tonne. Over time, increased production scale, technological advancements, and more developed supply chains could help reduce SAF costs and narrow the price gap with conventional aviation fuel.

How much SAF is produced currently and how much will be required to reach net zero CO2 emissions in 2050?

In 2026, global SAF production is expected to reach approximately 2.4 million tonnes (Mt), accounting for 0.8% of total annual jet fuel consumption. SAF production roughly doubled from 1 Mt in 2024 to 1.9 Mt in 2025, but growth is expected to slow in 2026.

To support the aviation sector’s pathway to net zero emissions by 2050, annual SAF supply will need to expand to around 500 Mt, requiring production to increase by more than 250 times over the coming decades. Achieving this scale-up will depend on unlocking the full potential of sustainable biomass feedstocks and prioritizing their use in sectors such as aviation, where decarbonization alternatives are limited. While the bio-SAF is expected to provide a significant share of future supply, it will have to be complemented by substantial volumes of e-SAF.

Achieving 500 Mt of SAF by 2050 will require coordinated action across the full SAF value chain and a broader energy system transformation. This includes policy frameworks that provide investment certainty, access to sustainable feedstocks and renewable energy, investment in fuel and energy infrastructure, effective technology deployment, and mechanisms to transfer risk across the SAF value chain.

What is “Book-and-Claim,” and how does it help decarbonize aviation?

Book-and-Claim (B&C) is a mechanism to account for and track the environmental benefits of SAF thanks to a robust chain of custody. It separates the environmental attributes from the physical SAF. This allows all SAF producers to sell to all airlines in the world, and it allows all airlines to buy SAF from any producer in the world – an instant global market that opens the SAF market to global competition, drives innovation, reduces market fragmentation, and ensures competitive prices. To ensure transparency, avoid double-counting, and link each claim to verified SAF use, these attributes need to be tracked through dedicated registries, such as the CADO SAF Registry.

What role do governments play in scaling SAF?

Governments play a critical role in scaling SAF, particularly in creating the policy and investment conditions needed to accelerate production, reduce costs, and support market development. Given that SAF production technologies and supply chains are still at very early stages of development, supportive government policies are essential to help bridge the price gap between SAF and conventional aviation fuel and provide long-term certainty for investors and producers.

Key measures may include production incentives, grants, loan guarantees, supportive regulatory frameworks, research and innovation support, and policies that facilitate access to feedstocks and infrastructure.

Governments also play an important role in promoting internationally harmonized sustainability and certification frameworks to support the development of a global SAF market. Governments should also support the development and recognition of global SAF book-and-claim systems, consistent with the purchase-based claiming approach allowed under CORSIA, to help create a more efficient, transparent, and globally connected SAF market.

IATA has developed the Net Zero Policy Roadmaps to support governments in this effort, providing a menu of policy options and practical measures that can help aviation achieve its decarbonization goals, including the scale-up of SAF production and deployment. Governments must also work through international bodies such as ICAO and mechanisms such as CORSIA to help ensure globally harmonized approaches to aviation decarbonization and the scale-up of SAF.

Importantly, governments should also consider policy sequencing as part of the broader energy transition. As highlighted in the IATA Energy Transition and System Transformation publication, effective sequencing of policies and investments is essential to avoid supply bottlenecks, infrastructure mismatches, and unintended market distortions. This includes aligning energy, industrial, transport, and climate policies to ensure that enabling conditions such as renewable energy availability, infrastructure development, technology readiness, workforce capabilities, and financing mechanisms evolve in a coordinated manner. A sequenced and systems-based policy approach can help accelerate SAF deployment while maintaining energy security, affordability, and competitiveness. Any SAF mandates should therefore be introduced only where the necessary market conditions, production capacity, infrastructure readiness, and supportive policy measures are sufficiently in place, in order to avoid unintended economic impacts, supply constraints, or disproportionate cost burdens on the aviation sector and consumers.

Our strategy towards net zero CO2 emissions

Achieving net zero CO2 emissions by 2050 will require a combination of maximum elimination of emissions at the source, offsetting and carbon capture technologies.

|

|